Arts & Culture

Lest we forget: Storing precious memories

On Anzac Day, we take a look at the untold story of Australia’s wartime accountants

Published 23 April 2017

The impending gloom engulfing Western Europe in the late 1930s as the world stumbled towards war brought with it many unexpected realities, along with opportunities for those with skills required by government.

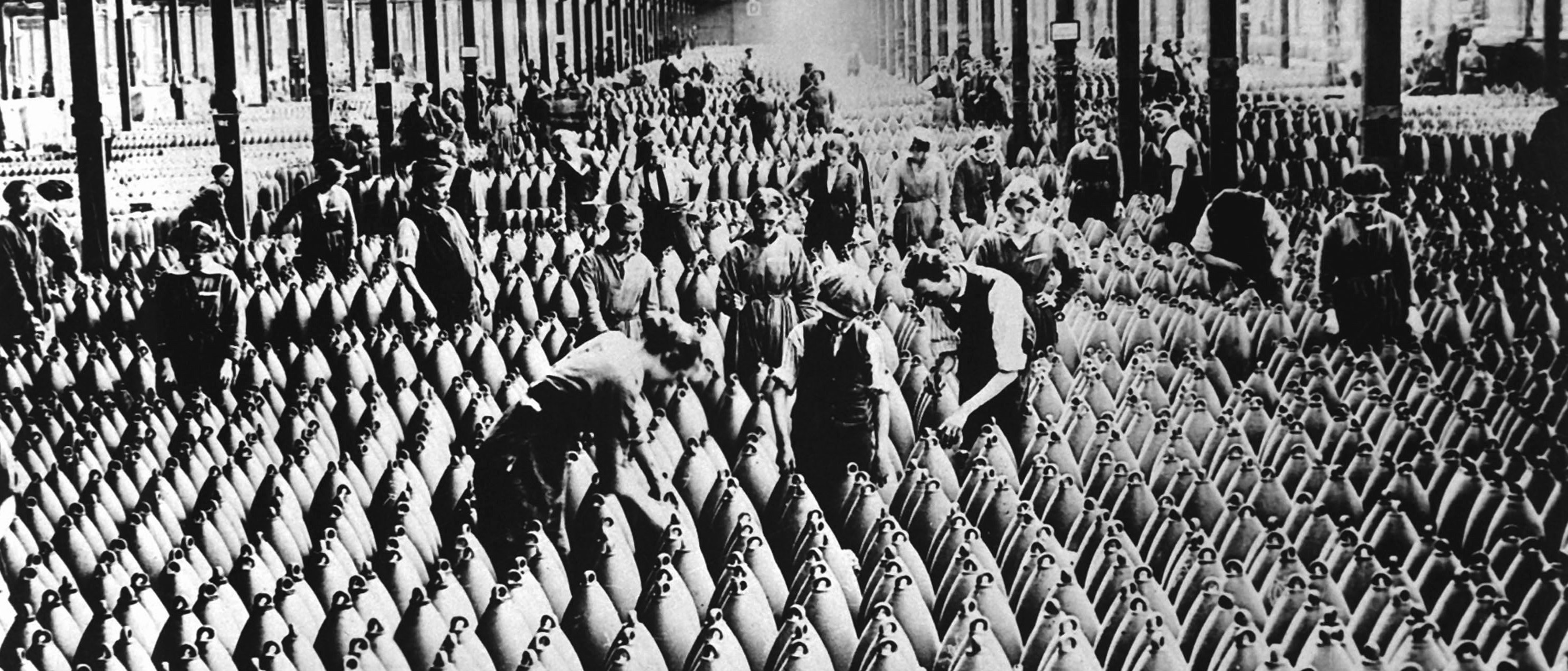

At this time, Australia received some galling advice from the British Government – the UK would be unable to supply munitions such as rifles, heavy and light artillery, and ordnance to its allies as they had done throughout the years of World War 1.

This decision was of particular concern to the Australian Federal Government.

Up to this point, munitions manufacturing had been confined to four government munitions factories, three in Victoria and one in country New South Wales. It was an arrangement consistent with an ideological position adopted by all governments since Federation that forbade the manufacture of munitions for profit.

The immensity of Whitehall’s advice and the potential consequences for Australia in the face of expected threats to the north from Japanese Imperial Forces caused a seismic shift in government policy. To enable self-sufficiency in the supply of munitions the Government decided, for the first time, to permit the manufacture of munitions for profit in private facilities known as war annexes.

Arts & Culture

Lest we forget: Storing precious memories

This strategy was handled through contracts written on a ‘cost-plus’ basis, an approach that attracted great controversy and was much maligned in the aftermath of the Great War when the British Government was accused of condoning war profiteering by the vast munitions trusts. The Australian Government was acutely aware of the vulnerability of the nation to the rapacious behaviour of war profiteers.

Cost plus contracts were structured with contractors remunerated on the basis of total manufacturing costs plus a margin of profit. Margin of profit could be mandated by government fiat or agreed by negotiation, but the real test came with the identification of costs the Government was prepared to reimburse.

As the Government of the day enjoyed the support of the business community it recognised early the potential political dangers of perceptions in the wider community that it was promoting or condoning excessive profits in a time of national emergency.

To encourage private interests to engage in war production, the Government decreed contractors should be rewarded on a reasonable basis and that the people of Australia should be required to pay fair and reasonable prices for the munitions. Incentives were weighted heavily in favour of the contractor unless some form of control was placed over costs to be reimbursed.

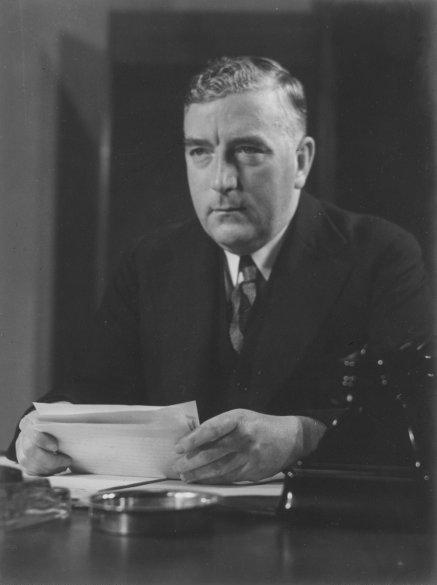

To deliver on this promise, in 1939 the Government turned to the Australian accounting profession for advice. The Prime Minister, R.G. Menzies, appointed a panel drawn from the senior ranks of the practicing and commercial elements of the profession.

Known as the Accountancy Advisory Panel in the Department of Supply and Development the panel included EV Nixon, Chairman, principal, Edwin V Nixon and Co., Chartered Accountants, Melbourne; LA Schumer, General Manager, Yellow Express Carriers Ltd., Melbourne; SW Griffith, principal, Jamieson, Griffith and Byatt, Chartered Accountants, Sydney; DJ Nolan, Assistant General Manager, Sydney County Council, Sydney and TD Hadley, principal, Offner, Hadley and Company, Chartered Accountants, Sydney.

Sir Edwin Nixon and Les Schumer were both part-time academics teaching accountancy at the University of Melbourne. Sir Edwin was also the first (part-time) head of the accounting discipline in the University and a member of the board of the Faculty of Commerce from 1924 to 1932.

The task given the panel was to review the pricing and profit levels related to manufacture of war-related products. This remit was expanded to include existing and potential methods to restrict prices to a fair and equitable rate for both parties.

Arts & Culture

Why Emmeline Pankhurst criticised her daughter

Not surprisingly this advice focused heavily on costing procedures in non-government establishments. At the time all contracting was done with a Standard Form Contract and the panel focused on this from the outset, immediately identifying the major deficiency in the general conditions as the lack of detail on reimbursable costs.

The panel’s short tenure lasted from August 1939 until July 1940 and it reported on five separate occasions.

In the first and third reports, the panel looked closely at the standard form contract. The second and fourth reports were site-specific investigations of Cockatoo Island Dockyard and Engineering Company in Sydney Harbour and De Havilland Aircraft Company at Mascot Airfield in Sydney. The use of contractors’ auditors for cost verification purposes made up the final report.

The summation of the first four reports resulted in the identification of Raw Materials and Direct Labour and a list of Overhead items that the Government should reimburse (inclusions) along with a further list of Overhead items that were specifically excluded (exclusions).

The advice provided in the first and third reports was distilled and subsequently formalised as a costing memorandum that was circulated widely within the munitions manufacturing industries. In providing this advice the panel was recommending a ‘specific identification of overhead costs model’ to establish manufactured costs upon which the margin of profit would be applied in order to establish the amount (price) the Government was prepared to reimburse.

The advice contrasted with standard contemporary costing orthodoxy that applied an ‘overhead application rate’ to determine total manufactured cost and was made in full knowledge of the need to limit the likelihood of profiteering by manipulating overhead.

Despite its short tenure, the panel was able to provide critical advice to Government at a crucial time in the history of the nation. The advice provided was the foundation of a costing system that was applied throughout the munitions manufacturing sector for the duration of the war.

In June 1940 it was subsumed by the Ministry of Munitions. Edwin Nixon, as chair of the panel, was appointed to the full-time post of Director of Finance in the new ministry, continuing the work of the panel as the ministry managed the expansion of munitions manufacturing capacity to levels unimagined before the outbreak of hostilities.

The Accountancy Advisory Panel in the Department of Supply and Development was one instance where the technical expertise of the accountancy profession was enlisted by government in the service of the nation during World War 2. A second panel established in the Department of Army in 1942 was charged with providing advice on efficiency and effectiveness of administration within the department.

In 1940 the Australian accounting profession created the Central Register of Accountants for National Service, the only known occasion where a profession has self-enlisted in a time of war to provide services at no cost to the nation.

Banner image: Shutterstock