Politics & Society

Maybe just think about who’s carrying the mental load at Christmas

As many of us struggle through the expensive holiday period, it seems financial relief may be coming – but perhaps not as swiftly as we want

Published 24 December 2025

Australian households are still reporting budget crunches ahead of Christmas 2025, despite headline inflation – one of the major contributors to the cost-of-living crisis – declining significantly in the last three years.

As we head into the festive period, many families will be watching their wallets closely as they seek to strike a balance between saving for the essentials and increased holiday spending. But what has led us here?

Annual inflation in Australia reached a high of nearly 8 per cent in late 2022, driven by a combination of global supply disruptions, strong demand and rapid increases in housing-related costs.

By mid‑2025, that rate had dropped to a little above 2 per cent, well within the Reserve Bank’s 2–3 per cent target range.

The problem is that the big initial decrease in headline inflation coincided with relative price rises in big-ticket expenses like housing and energy – expenses that take up a large share of household budgets.

Politics & Society

Maybe just think about who’s carrying the mental load at Christmas

Temporary electricity rebates in 2024–25 offered brief respite, but with these rebates now scaled back or exhausted, out‑of‑pocket electricity bills are rising once again.

At the same time, higher council rates, insurance premiums and persistent rental increases are keeping housing costs elevated, even as some other categories stabilise.

This recent shift is even clearer when we look at monthly inflation stats like the Melbourne Institute Monthly Inflation gauge, as well as underlying measures like trimmed-mean inflation - so we can see that price pressures might be a little harder to shift than first thought.

The momentum swing in inflation in the second half of the year also changed which Australians were feeling the biggest impacts of cost-of-living pressures.

Living Cost Indexes, which provide a clearer picture of which households are most affected, showed some pressure has been lifted off employee households and homeowners, who often put a lot of their income towards mortgage repayments.

In contrast, prices of essentials continue to rise, which is most prominently felt by pensioners and other households reliant on government payments.

This effect is felt by renters too, with the cost of rent increasing in capital cities, and vacancy rates still relatively low.

For these groups, the overall pace of cost-of-living growth has remained comparatively high, and this can mean there’s less available for those well-deserved holiday treats.

All of this will naturally shape how households approach the Christmas period.

The end of the year typically coincides with increased spending on gifts, travel and social events, while regular bills still need to be paid.

While retail data suggest that nominal spending has been growing, much of this reflects higher prices and population growth, rather than an increased volume of spending.

Households appear to be rebalancing towards essential items and away from discretionary purchases.

Over the course of 2025, household spending on non-discretionary items rose by a little over 5 per cent, compared to an increase of 3.6 per cent for discretionary items. How this plays out during the holiday period remains to be seen.

And we can’t ignore the role of financial products in all of this.

Politics & Society

New business models could help save Australia from its housing crisis

Buy now, pay later services and the continued use of credit cards can also increase vulnerability, especially if incomes are disrupted or interest rates remain high.

For lower‑income households with little financial buffer, the combination of seasonal spending and elevated living costs can result in greater reliance on short‑term credit or support services.

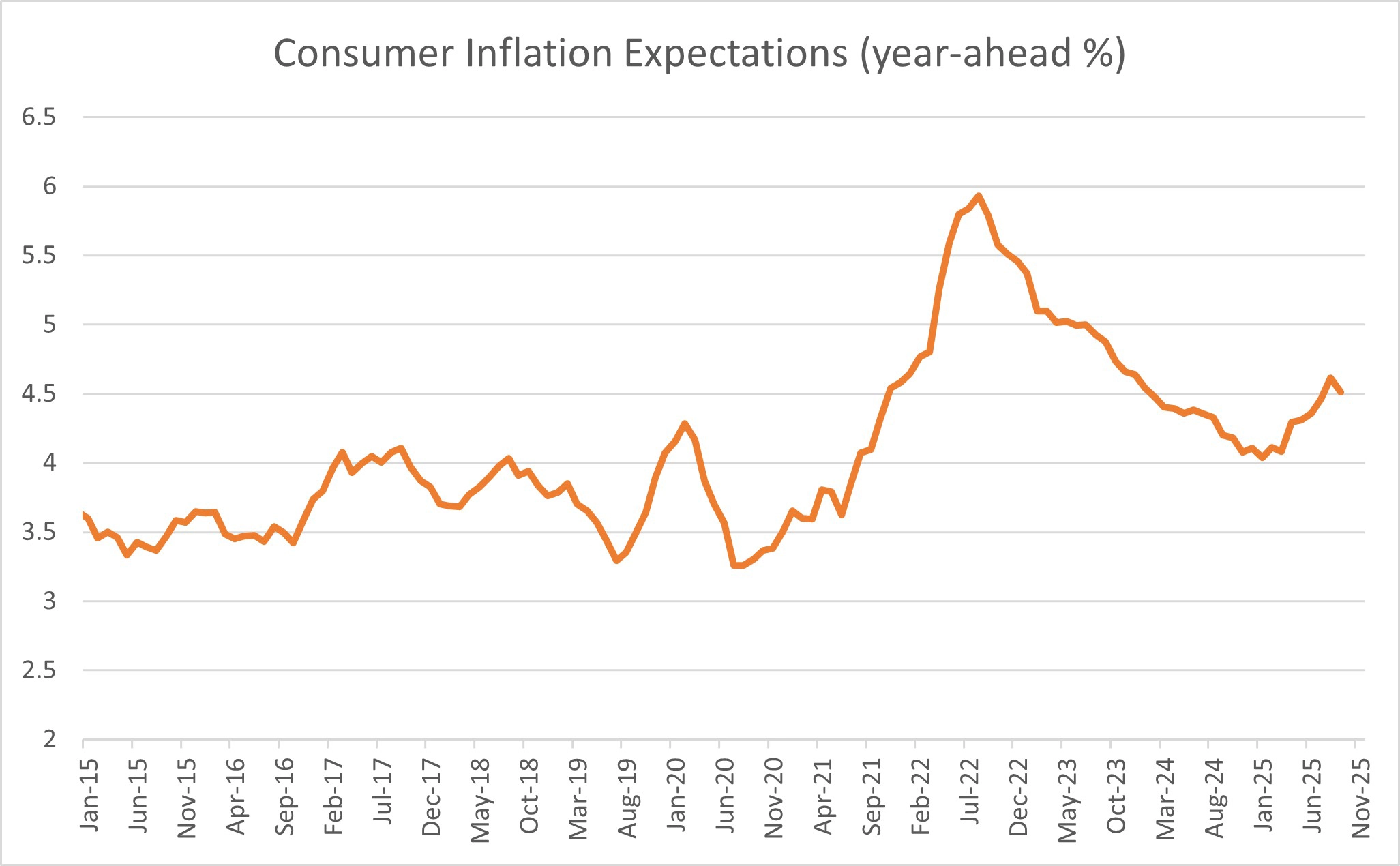

Past Christmas and into the New Year, consumers are telling us they’re expecting higher inflation in the next 12 months than they were at the start of 2025.

In the first quarter of 2025, consumers expected year-ahead inflation of about 4.1 per cent. In the three months to November, this rose to 4.7 per cent.

It’s clear that Australians have noticed the inflation momentum swing over the last few months.

From a cost-of-living perspective, three issues stand out.

First, energy prices are likely to stay a key source of uncertainty, with unwinding electricity rebates making these bills an increasingly large proportion of household budgets.

Second, wage and income dynamics will be critical. As a result of the recent inflation spike, the prospect of negative real wages in at least part of 2026 still looms, likely sustaining cost-of-living pressures.

Politics & Society

Have yourself a very thrifty Christmas

Third, many will be keeping an eye on interest rates, as their trajectory will influence how 2026 plays out for mortgagors and renters.

A prolonged period of higher rates would keep repayments elevated for existing borrowers, but a faster‑than‑expected easing cycle, while helping mortgage holders, might raise broader inflationary pressure.

Overall, the outlook for 2026 is one of gradual adjustment rather than abrupt relief.

Inflation is expected to move closer to the Reserve Bank’s target band but is likely to remain elevated in the first half of the year. So an easing is likely coming, but this could still be months away.

Real wages will likely shift from negative to positive over the course of the year, which will also be a much-needed shift in purchasing power.

While there’s a handful of positive shifts that will hopefully ease the pressure, the challenge for policy remains to manage inflation risks while designing support that recognises how unevenly the cost‑of‑living pressures of recent years have been distributed.