Politics & Society

Where to now for Australian property?

As the world faces one of the fastest and largest global economic contractions in living memory, Australia’s house prices are likely to fall for months – possibly years

Published 28 May 2020

The COVID-19 pandemic has swiftly upended lives, jobs and economies – but we’re yet to see the full impact on housing.

In a time of enormous uncertainty, understanding what’s happening in the housing market is important, not least because housing is the biggest source of wealth for most Australian households.

The total value of residential property in Australia is more than triple that of publicly listed securities, according to the Australian Bureau of Statistics (ABS) and the Australian Stock Exchange (ASX).

Complementing government measures to protect jobs and incomes, banks have paused mortgage repayments, landlords have deferred rents and, for the moment, there’s a moratorium on evictions.

But with restrictions beginning to lift, people have started returning to auctions.

Politics & Society

Where to now for Australian property?

So, what is the pandemic likely to mean for house prices and values in coming months and years?

The COVID-19 pandemic has caused one of the fastest and largest global economic contractions in living memory. In response, financial markets have rapidly re-priced securities like stocks and bonds.

House prices usually take longer to reflect what is happening elsewhere in the economy for a number of reasons. Essentially, houses are harder to buy and sell than stocks and bonds, houses differ greatly from one to the next, and people value houses as more than just investments.

This also means that house prices are more predictable than other types of assets; and how far and how fast stock prices have fallen today can also indicate what is in store for house prices in the coming months.

Our team used data from financial companies listed on the ASX to forecast house prices over the June and September quarters of 2020.

Health & Medicine

Australian homes on the line

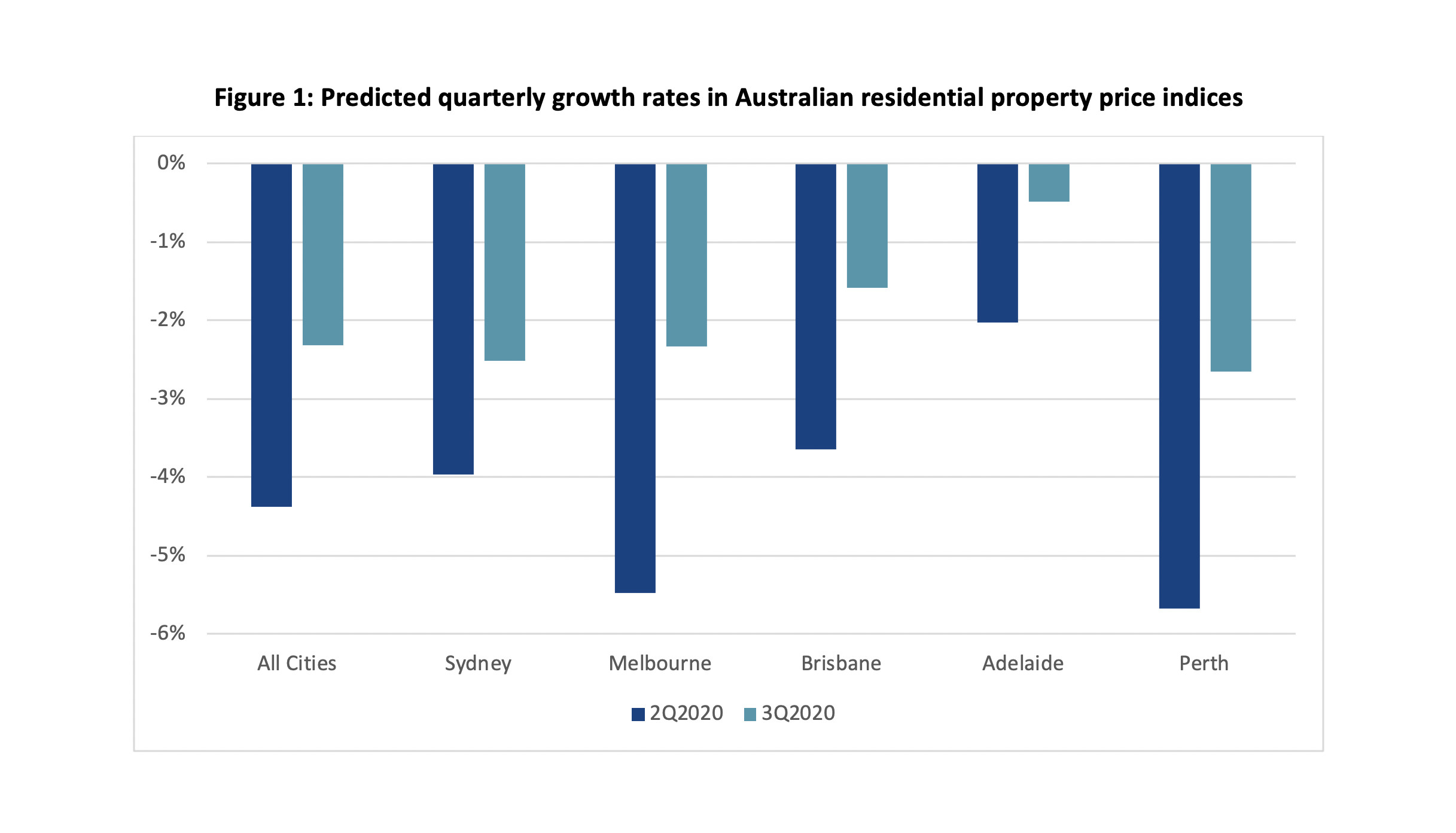

Our models predict that residential property prices across all capital cities will fall by 4.4 per cent over the June quarter and by another 2.3 per cent in the September quarter of 2020.

Sydney prices are predicted to fall by 4 per cent in the June quarter and about 2.5 per cent in the September quarter.

Falls in prices in Brisbane and Adelaide are tipped to be less severe but in Melbourne and Perth, our models predict falls of around 5.5 per cent and 2.5 per cent in the June and September quarters, respectively.

WHAT THIS MEANS FOR HOUSEHOLDS WITH MORTGAGES

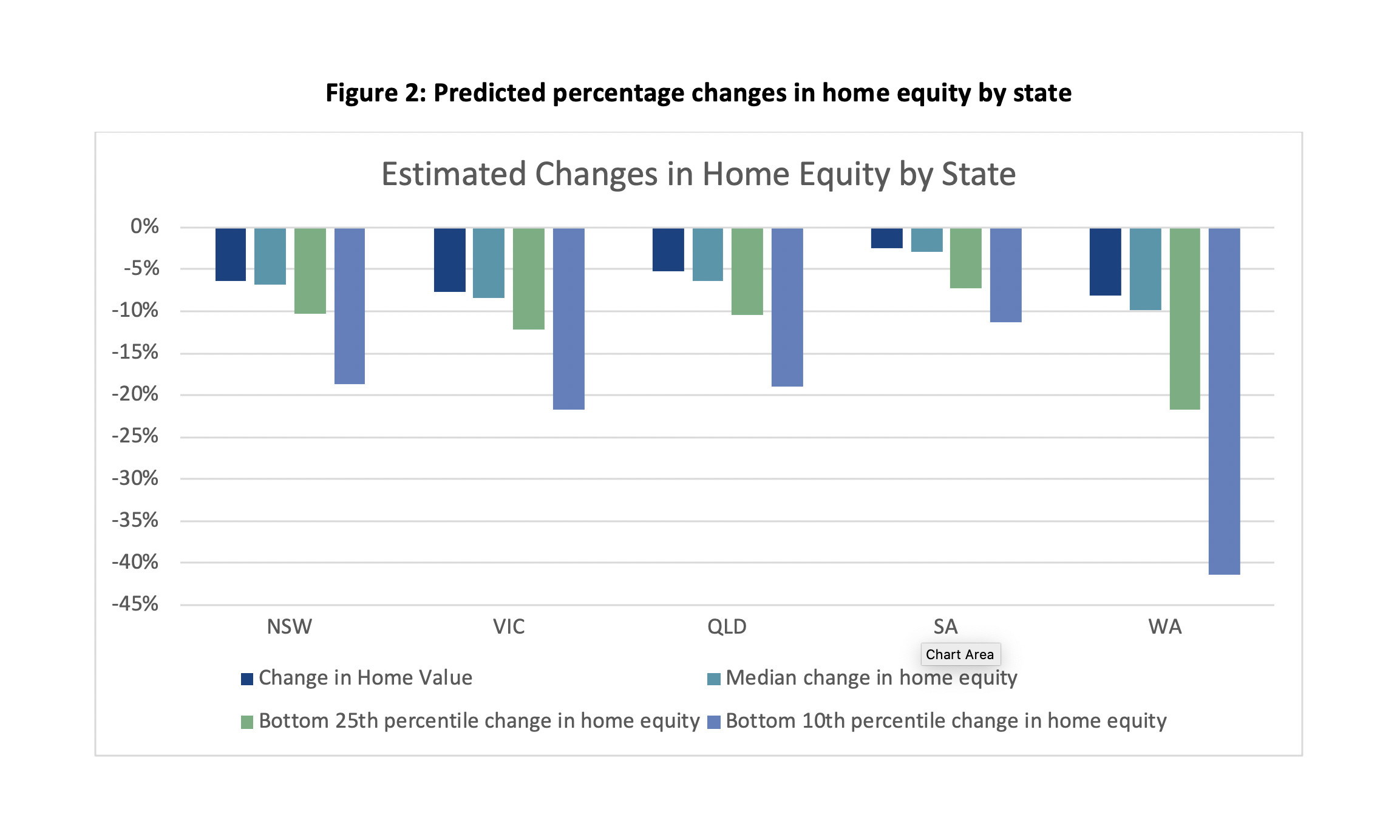

We also calculated the impact on home equity – the difference between a home’s value and the amount of debt borrowed against it. If you were to sell your home today, home equity is the cash you would receive from the buyer after repaying all outstanding debts on the home.

Using data from 2018’s Household, Income and Labour Dynamics in Australia (HILDA) survey, including self-reported house values and debt levels, we adjusted home values to calculate the change in home equity between March and September 2020.

Most households have only a small amount of borrowings against their home and are generally in good positions to withstand a fall in home values.

However, households that have borrowed more money will feel the impact on their home equity more.

In Sydney, Melbourne and Brisbane, we calculate that a quarter of households will see a fall in equity of 10 per cent or more.

Health & Medicine

The young Australians hit hard during COVID-19

In Adelaide, the figures are less severe but for Perth one quarter of households face a reduction in home equity of 20 per cent or more. This is because the Perth property market is more exposed to movements in stock prices, and average household debt levels are higher relative to home values.

To forecast Australia’s home prices in the June and September quarters, our team used a statistical technique called Mixed Data Sampling (or MIDAS).

MIDAS techniques are designed to produce forecasts of a low-frequency (for example, quarterly) variable using high-frequency (that is monthly, daily or even hourly) predictors.

This framework helps us to develop forecasts for growth rates in ABS Australian residential property price indices, which are observed quarterly and with a two-month lag.

We used the daily returns of the S&P / ASX 200 Financials Sector index, which includes companies involved in things like banking, mortgage finance, consumer finance, asset management and real estate, up to May 2020.

We don’t claim that our models produce the best possible forecasts of home values. As with all models, particularly at the moment, we’ve had to make a number of assumptions that don’t always hold true in the real world.

Business & Economics

Who’s hit hardest by the COVID-19 economic shutdown?

Nevertheless, our predictions suggest that house prices and values will fall over coming months and possibly years. Our analysis suggests that while many households are well equipped to deal with this, a large fraction have very significant exposure and are likely to suffer significant wealth destruction.

This also has important implications for Australia’s Gross Domestic Product (GDP), because changes in wealth have meaningful impacts on consumption and economic growth.

In coming months, policies that support housing markets, like low interest rates, mortgage relief and support for first home buyers, could play an important role in mitigating these negative effects on the wealth of Australian homeowners.

Banner: Getty Images