Politics & Society

Budget hits political reset

The upcoming federal election could be fought over proposed income tax cuts, but what’s the main difference between the Coalition and Labor’s plans for taxation?

Published 9 May 2019

Personal income tax, the taxes levied on individuals’ income from wages and capital, collected $A206 billion in 2017-18. This represents roughly a half of total Commonwealth tax revenue, and 11 per cent of national income.

In their overall approach to personal income tax, the Coalition is largely keeping the status quo intact while the Labor Party aims to increase the taxes collected on income from capital received from asset classes that are more commonly held by higher income and higher net-worth individuals.

For the next three years, both parties propose similar, but not identical, reductions in personal income tax rates for low- and middle-income taxpayers. However, these changes do little more than offset the effect of higher nominal incomes sneakily increasing average tax rates for all, or so-called ‘bracket creep’.

The main difference between the two major parties is in their approach to taxation on income from capital.

Politics & Society

Budget hits political reset

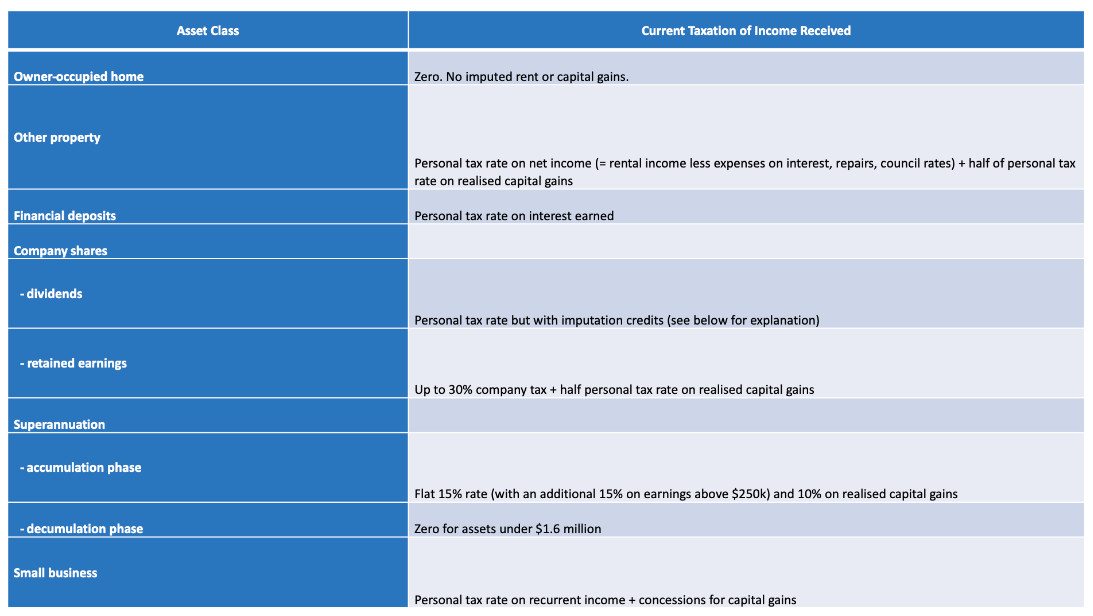

Capital income tax is the tax on income received from owning various classes of capital such as property, company shares and superannuation.

Very different tax systems and effective tax rates are levied on the capital income received by individuals for investments in their own home, other property, financial deposits, company shares and superannuation.

The different tax treatments of different categories of capital income is summarised in the table below:

Interest income on financial deposits and dividends are taxed at the personal tax rate in the same way as wages and salaries. At the other extreme, there is no income tax on the returns from investment in the owner-occupied home, nor on income earned on superannuation when in retirement.

The combination of negative gearing and the half tax rate on capital gains imposes an effective income tax rate on investment in other property between these extremes.

The very different effective tax burdens on the different household saving and investment options raise concerns of both tax neutrality and equity.

Business & Economics

Good policy vs poor politics at Outlook 2018

The wide range of different tax burdens encourage the reallocation of savings from the higher taxed options, including financial deposits and shares with high dividend yields, to the lower taxed options such as bigger and better homes and superannuation for those on high incomes.

The capital income tax concessions favour those with higher incomes and higher saving rates, and they favour older generations relative to the young.

While the Coalition proposes no changes in the current capital taxation scheme, Labor proposes a couple of key changes to increase the overall tax collected.

An imputation, or franked, credit is a tax credit that comes along with any dividend income that the company has already paid on (generally at the 30 per cent corporate income flat tax rate). Such dividends are called ‘franked dividends’.

For example, if one has a low taxable income, recipients of a franked dividend would be refunded the difference between the company tax paid and their personal tax rate; and if one has a high income and a tax rate above 30 per cent, additional personal income tax would be payable. In net, the effective tax on dividends is the individual’s personal income tax rate.

The most controversial aspect of this system is that even individuals who pay no personal income tax still receive the 30 per cent tax refund (as a payment from the government) on the corporate tax paid by the company that paid out the franked dividend.

Politics & Society

Competition policy: An election issue?

The Coalition proposes to retain the current imputation system and refundable franking credits.

Labor, by contrast, proposes to end refundable franking credits for all except those on social security payments, including the Age Pension.

The change will not affect most middle and all high-income earners who have income tax rates of 30 per cent and above. But, it will increase the tax paid on dividends for many with average tax rates below 30 per cent.

Individuals facing higher tax burdens on savings invested in company shares includes retirees with self-managed super funds, some of working age with self-managed super funds, and others with low taxable incomes largely consisting of franked dividends.

These changes will impact tax efficiency and equity for those affected. Their impact will be to:

Increase the overall tax burden on those who invest their savings in shares relative to financial deposits

Further disadvantage shares and their holders relative to savings invested in own homes

Place higher effective tax rates on self-managed super funds relative to industry and retail super funds who can fully utilise franking credits

Politics & Society

2019 Budget: Not just another budget reply

Relative to the tax-free treatment of income generated by investing in owner occupied homes, income generated from investments in second properties is subject to income tax, but with concessions.

Labor proposes to reduce these tax concessions by:

Restricting negative gearing (rent received less expenses) as an offset only to other property income rather than the current allowance as a deduction against all other forms of taxable income

Increasing the capital gains tax rate from the current 0.5 of the personal tax rate to 0.75 (but they will retain current arrangements for new buildings and grandfather current property holdings)

Data from the Australian Tax Office indicates that many more taxpayers on middle incomes than high incomes will be affected by the higher property income taxes, but a higher share of higher income taxpayers will be affected, and most of the additional tax revenue will be collected from higher income taxpayers.

In terms of tax distortions to the allocation of saving and investment across different options, and equity across individuals with different savings mixes, effects of the property income tax changes are mixed.

Relative to the current arrangements the favourable income tax treatment of savings invested in own homes and superannuation is increased, and the tax concessions for savings allocated to other property relative to shares and financial deposits is reduced.

Business & Economics

2019 Budget: The Verdict Part 1

Labor proposes other changes to raise additional revenue. These include: imposition of a flat 30 per cent tax on income distributed by discretionary trusts to reduce one of several tax-reducing income splitting strategies available to small business; and, reductions in eligible contributions of savings allocated to the low-taxed superannuation.

A version of this article first appeared on Election Watch.

Banner: Shutterstock